New York based market expertise and investment consulting firm Arrowhead Business and Investment Decisions published a report on the potential of South Boulder Mines and its mining prospects. Find below an excpert and a link to the entire report.

[wikichart align="right" ticker="asx:stb" showannotations="true" livequote="true" startdate="22-08-2010" enddate="22-02-2011" width="300" height="245"]

South Boulder Mines Limited is an Australian-listed exploration and development company focusing on multiple gold, nickel and fertilizer prospects primarily located in Western Australia and Eritrea in North East of Africa.

One of South Boulder’s main areas of focus is on its Duketon Greenstone Belt projects which contain the exciting new Rosie NiCu-PGE discovery. The company owns 100% of all gold prospects and participates in a farm-out Joint Venture with Independence Group NL (earning 70%) for nickel sulphide prospects within the same area.

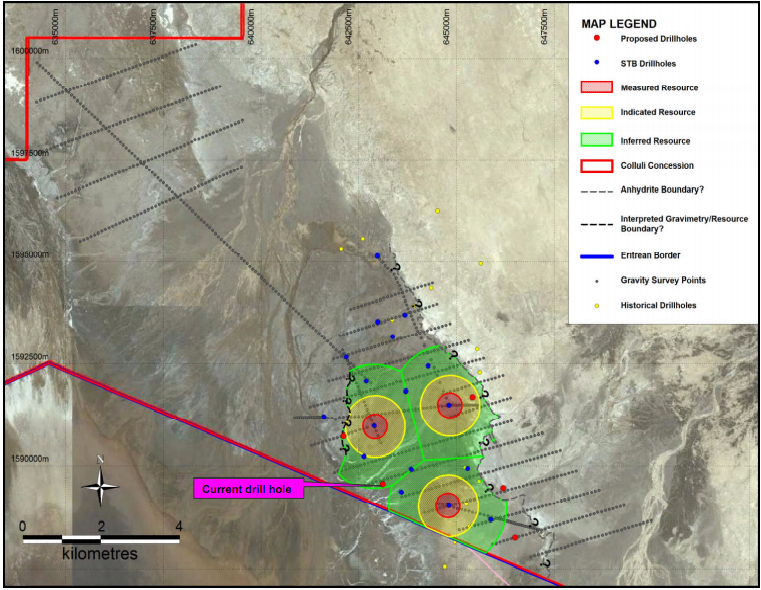

South Boulder Mines Ltd has a 100% interest in the Colluli Potash Project located in the Danakil Depression region of Eritrea (Africa), approximately 200km south east of the Capital Asmara. In January 2011, South Boulder announced the maiden JORC/43-101 compliant resource estimate for the Colluli Potash project. It reported a Measured, Indicated and Inferred resource of about 548MT @ 19% KCl including 119MT @ 23% KCl (total contained potash of 102MT) located at <100m depth. It plans to increase the exploration target to 750MT – 1250 MT @ 18-20% KCl including 450MT – 750MT @ 20-23% KCl in the coming quarters.

South Boulder is currently conducting an engineering scoping study to ascertain the optimum potash processing capacity from 1MT to 10MT per annum. Arrowhead believes that this is a significant landmark which reduces the resource risk and improves the upside potential for the company.

South Boulder also has three (90-100%) owned fertilizer exploration projects in Western Australia. Given due diligence and valuation estimations based on discounted cash flow method, Arrowhead believes that South Boulder mines limited fair share value lies in the AS$6.25 to AS$29.95 bracket. iv This valuation is based solely on the Duketon Nickel and Eritrean Potash project and does not take account of the potential value of the company’s Terminator Gold prospect. We have also presented a comparable valuation based on Enterprise Value/resource and Enterprise Value /proposed capacity to ascertain the value the Nickel and Potash prospects respectively.

South Boulder Mines - Arrowhead BID Due Dillegence and Valuation Report

Please find below an excerpt from an interesting article by Dr. Alex Cowie in ‘Diggers and Drillers’ about South Boulder Mines, Eritrea, the Red Sea and the future potential of potash in terms of increasing global demand for fertilizer products needed to improve crop efficiency and agricultural output.

Please find below an excerpt from an interesting article by Dr. Alex Cowie in ‘Diggers and Drillers’ about South Boulder Mines, Eritrea, the Red Sea and the future potential of potash in terms of increasing global demand for fertilizer products needed to improve crop efficiency and agricultural output.

+0.00%

+0.00% +0.00%

+0.00% +0.00%

+0.00% +4.65%

+4.65% +0.00%

+0.00% +4.94%

+4.94% +0.82%

+0.82% -6.67%

-6.67% +0.00%

+0.00% +0.00%

+0.00% +0.00%

+0.00%